-

[경제] (블룸버그) 투자자들은 강력한 미국 소비가 곧 벽에 부딪힐 것이라고 생각한다2023.09.12 PM 02:14

블룸버그 기사 요약 (ChatGPT)

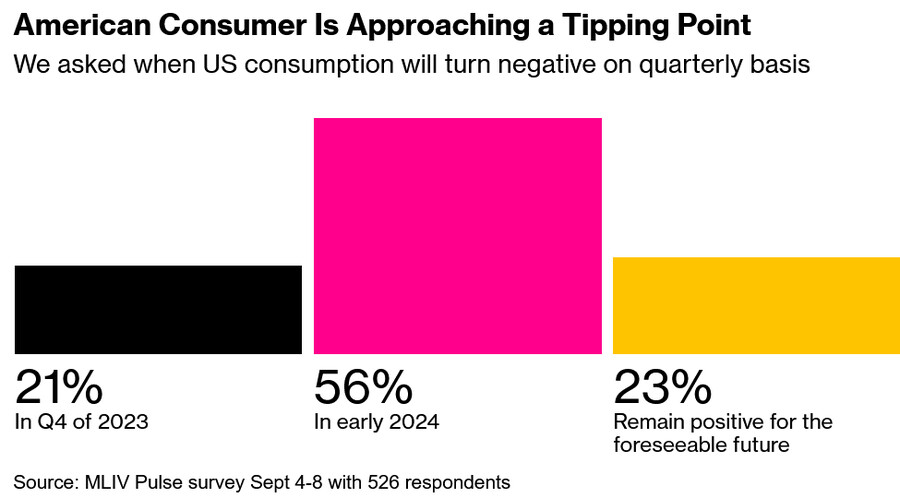

블룸버그 마켓 라이브 펄스 설문조사에 따르면, 미국 소비자는 2024년 초에 지출을 줄일 것으로 예상됩니다. 이러한 예상이 맞다면, 팬데믹 이후 최초로 소비가 전분기 대비 감소하는 것입니다. 일부 사람들은 이러한 소비 위축이 올해 마지막 분기에도 발생할 수 있다고 예상하고 있습니다. 이는 높은 차입 비용이 가계 예산을 약화시키고 팬데믹 시대의 저축이 줄어들기 때문입니다.

이 설문 결과는 여름 내내 미국 주식 시장에서 널리 퍼진 낙관론과는 대조됩니다. 이는 냉각되는 인플레이션과 낮은 실업률과 같은 요인에 의해 주도되었습니다. 소비자 지출이 감소하고 경제가 성장을 멈추면 이미 7월 말 고점을 벗어난 주식 시장이 더 하락할 수 있습니다.

최근 가계 지출이 증가하면서 미국 경제의 현재 강세는 블록버스터 영화(바벤하이머)와 콘서트 투어(테일러 스위프트, 비욘세)와 같은 일회성 요인에 의해 주도되는 일시적인 급증으로 보는 시각이 있습니다.. 블룸버그 이코노믹스의 Anna Wong과 같은 경제학자들은 올해 말에 경기 침체가 시작될 것으로 예측합니다.

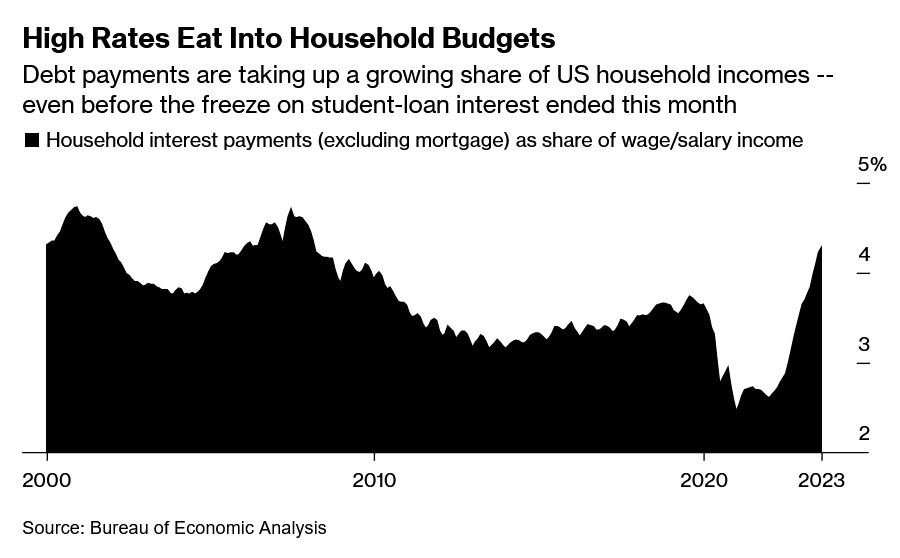

일부 분석가들은 골드만삭스와 같이 2024년에도 소비자가 꾸준한 일자리 증가와 임금 인상 덕분에 계속해서 선전할 것으로 예상하지만, 우려도 있습니다. 샌프란시스코 연방준비은행은 소비자들이 인플레이션 상승에 대처하는 데 도움이 된 초과 저축이 곧 고갈될 수 있다고 경고합니다. 신용카드와 자동차 대출의 연체율이 증가하고 있으며, 팬데믹으로 유예되었던 연방 학자금 대출 상환이 재개되는 것은 또 다른 도전입니다.

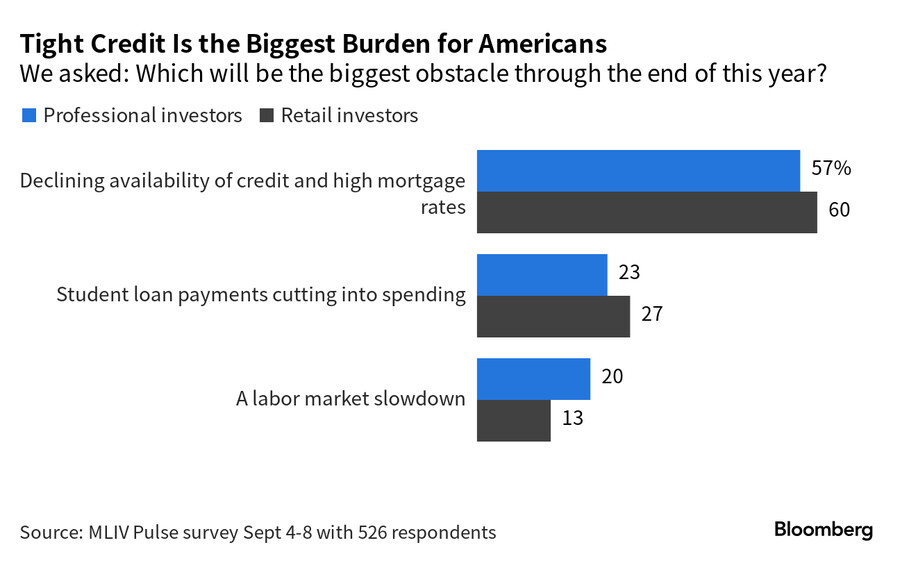

소비자들이 앞으로 몇 달 동안 직면하게 될 주요한 도전은 신용(대출)에 대한 접근성과 이자 비용, 특히 20년 만에 가장 높은 모기지 금리입니다. 설문조사에 참여한 투자자들은 자동차와 소매 업종 주식이 저축 감소와 소비자 신용 제약에 가장 취약하다고 믿고 있습니다. 이는 시장 가격에 아직 완전히 반영되지 않은 우려입니다.

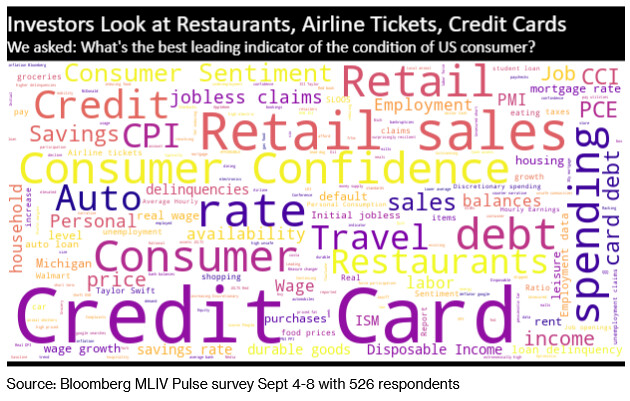

전반적으로 미국 소비자의 미래 지출 행동에 대한 불확실성은 투자자들에게 주요 관심사이며, 그들은 전통적인 측정 지표(소매 판매, 신용카드 연체율) 이외의 다양한 지표(항공권 구매, 애완동물 입양, BNPL 할부 구매)를 사용하여 소비 상황을 평가하고 있습니다. 포스트 팬데믹 환경에서 경제 및 시장 환경은 복잡하고 예측하기 어려우며, 전개되는데 더 오랜 시간이 걸립니다.

================================================================

The Mighty American Consumer Is About to Hit a Wall, Investors Say

Key engine of US growth is poised to sputter in early 2024, according to survey respondents.

2023년 8월 15일 화요일 미국 일리노이주 시카고 매그니피센트 마일 쇼핑가의 쇼핑객들

Photographer: Jamie Kelter Davis/Bloomberg

By Reade Pickert and Vildana Hajric

2023년 9월 11일 오전 9:00 GMT+9

Updated on 2023년 9월 11일 오후 9:15 GMT+9

After staving off recession for longer than many thought possible, the US consumer is finally about to crack, according to Bloomberg’s latest Markets Live Pulse survey.

More than half of 526 respondents said that personal consumption — the most important driver of economic growth — will shrink in early 2024, which would be the first quarterly decline since the onset of the pandemic. Another 21% said the reversal will happen even sooner, in the last quarter of this year, as high borrowing costs eat into household budgets while Covid-era savings run down.

The finding is at odds with the optimism that’s permeated US equity markets for most of the summer, as cooling inflation and low unemployment bolstered hopes for a so-called soft landing. Should the economy stop growing — a scenario that’s quite likely if consumer spending contracts — it could mean more downside for stocks, which have already slipped from late-July highs.

“The likelihood of a soft landing, falling inflation, an end to Fed tightening, a peak in interest rates, a stable dollar, stable oil prices — all those things helped drive the market up,” says Alec Young, chief investment strategist at MAPsignals. “If the market loses confidence in that scenario, then stocks are vulnerable.”

‘It Is Not Sustainable’

Right now, the US economy appears to be speeding up rather than stalling. Growth is forecast to accelerate in the third quarter on the back of a recent pickup in household spending, which jumped in July by the most in six months.

To some analysts, it looks a bit like a last hurrah.

“The big question is: Is this strength in consumption sustainable?” says Anna Wong, Bloomberg Economics’ chief US economist, who expects a recession to start by year-end. “It is not sustainable, because it’s driven by these one-off factors” – notably a summer splurge on blockbuster movies and concert tours.

The enduring strength of the US job market has propped up household spending in the face of the biggest price increases in decades. It’s led some analysts to push out their expectations for a recession — or even scrap them altogether.

Economists at Goldman Sachs Group Inc. expect the consumer to outperform yet again in 2024 — and keep the economy growing — amid steady job growth and pay hikes that beat inflation.

‘Really Struggling’

But there are plenty of headwinds looming.

Researchers at the Federal Reserve Bank of San Francisco say the excess savings that have helped consumers get through the price spike will run out in the current quarter — a sentiment that three-quarters of the MLIV Pulse respondents agreed with.

“There’s increasingly an issue where the lower end of the income and wealth spectrum is really struggling with the accumulated inflation of the last couple years,” while wealthier Americans are still cushioned by savings and asset appreciation, said Thomas Simons, Jefferies’ US economist.

In the aggregate, consumers have been able to bend under the weight of higher prices, he said. “But there will come a point where that’s no longer feasible.”

Delinquency rates on credit cards and auto loans are rising, as households feel the financial squeeze after the Fed raised interest rates by more than 5 percentage points.

And another kind of debt — student loans — is about to come due again for millions of Americans who benefited from the pandemic freeze on repayments.

A majority of investors in the MLIV Pulse survey pointed to the declining availability and soaring cost of credit — mortgage rates are near two-decade highs — as the biggest obstacle for consumers in the coming months.

Some three-quarters of respondents said auto or retail stocks are the most vulnerable to declining excess savings and tighter consumer credit – a concern that’s not entirely priced in by the markets. While General Motors Co. and Ford Motor Co. have essentially missed out on this year’s wider stock rally, Tesla Inc. more than doubled in value.

‘Just Taking Longer’

Since the economy’s fate hinges on what US consumers will do next, investors are looking in all kinds of places for the answer.

Asked what they consider a good leading indicator, MLIV Pulse respondents pointed to everything from the most standard measures – like retail sales or credit-card delinquencies — to airline bookings, pet adoptions, and the use of “Buy Now Pay Later” installment plans.

That’s perhaps because conventional guides have often proved to be unreliable amid the turbulence of the past few years.

“The traditional playbook for the economy and markets is challenging in this post-pandemic environment,” said Keith Lerner, co-chief investment officer at Truist Wealth. “Things are just taking longer to play out.”

user error : Error. B.