-

[경제] (블룸버그) 원유시장 CTA가 움직이고 있다2023.12.02 PM 03:28

- 최근 원유시장 변동성 증가는 CTA를 통한 Systematic Trading의 증가 영향, 이로 인해 2023년에만 선물가격이 하루에 $2 이상씩 161번 움직이면서, 전년대비 엄청나게 증가

- CTA 거래는 추세를 따르는것처럼 보이지만, 실제로는 추세를 과장하기 때문에, 올해 유가 변동성 확대는 CTA전략에 따른 자동거래에 의해서 심화되었음.

- Bloomberg, 수요와 공급의 펀더멘털이 여전히 전반적인 상품가격 주기를 좌우하고는 있지만, 원유선물거래 시장이 투기세력에 의해 지배되고 있으며, 실물시장과의 단절을 초래하고 있음

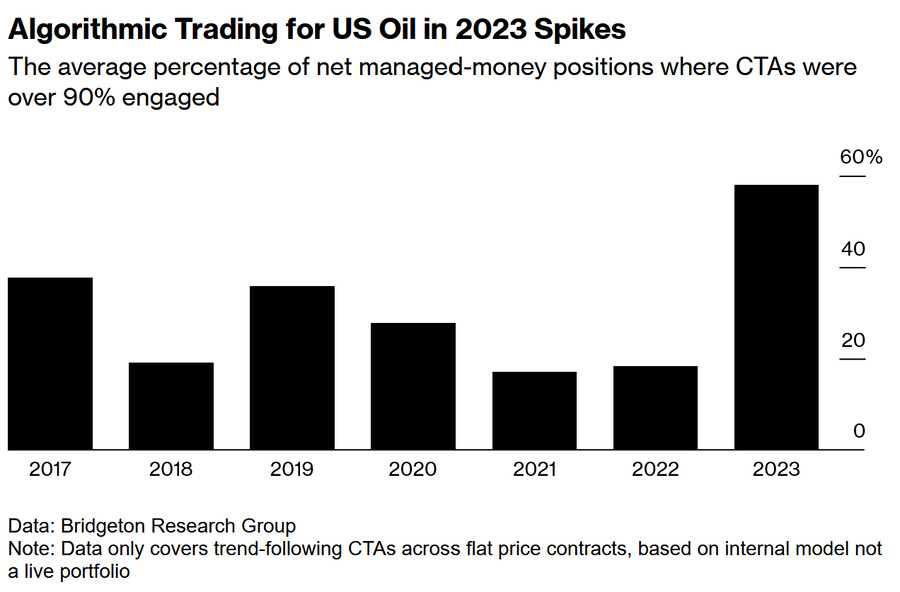

- Bridgeton Research, 원유선물시장내 순거래량의 60%가 Computer-generated trades가 차지함.

- JPMorgan & TD Bank, 전체 거래량중 CTA거래가 차지하는 대략적인 비중이 평균적으로 하루 평균 원유거래의 70% 차지

- CTA를 통해 원유 거래를 하는 기관들의 수익률이 계속 증가하면서, CTA 운용자산은 지속적으로 확장 중

- 한화투자증권 Global S&T 이효민 -

===================================

(Bloomberg) Oil’s Wild Ride Is Driven by a Disruptive Band of Bot Traders

An opaque group of algorithmic money managers have seized control of the oil market.

Illustrator: Joseph Gough

By Devika Krishna Kumar and Julia Fanzeres

2023년 12월 1일 오전 9:00 GMT+9

Trading oil has perhaps never been more of a roller coaster ride than it is today.

Just in the past two months, prices threatened to reach $100 per barrel, only to whipsaw into the $70s. On one day in October, they swung as much as 6%. And so far in 2023, futures have lurched by more than $2 a day 161 times, a massive jump from previous years.

What’s happening can’t be entirely explained by OPEC’s machinations, or war in the Middle East. While supply-and-demand fundamentals still dictate overall commodity price cycles, the day-to-day business of trading crude futures is increasingly dominated by speculative forces, fueling volatility and driving a disconnect between physical and paper markets.

And it’s not just speculators in general — traders are pointing the finger at an opaque group of algorithmic money managers known as commodity trading advisors.

Despite their mundane name, CTAs have emerged as a powerful force in the oil market. Though they comprise just one-fifth of managed money participants in US oil, CTAs made up nearly 60% of the group’s net trading volume this year by some measures, according to Bridgeton Research Group, which provides analytics on computer-generated trades. That’s the biggest share the group has held in data going back to 2017.

While it’s hard to quantify how much of total trading volumes are controlled by CTAs, algos more broadly are responsible for as much as 70% of crude trades on an average day, according to data from TD Bank and JPMorgan.

“You would be absolutely shocked how large their p-ositions are,” said Ilia Bouchouev, a former trader and managing partner at Pentathlon Investments who teaches at New York University. “They are probably bigger than BP, Shell and Koch combined.”

This year’s volatile price swings are being intensified by these bots, according to interviews with more than a dozen traders, analysts and money managers who work in the oil market. They’ve roiled commodities from gasoline to gold, sidelined traditional investors, drawn the ire of OPEC and even raised eyebrows at the White House.

CTAs are loosely labeled as an individual or organization that advises on the trading of futures, options or swaps. But those in the know say most are defined by their trading strategies: computer-driven and rules-based, with relatively limited time horizons.

What makes algorithmic CTAs so destabilizing is that they’re typically trend followers — and trend exaggerators. When prices go down, they sell, driving them even lower. And, more troubling for consumers, the same is true on the upside.

Some analysts say CTAs contributed to overvaluing oil by as much as $7 a barrel during a recent rally. And White House officials believe they played a significant role in price run-ups during the course of 2023, according to a person familiar with the matter.

Even $1 or $2 added to the price of a barrel filters down to consumers through higher fuel costs at a time when energy-driven inflation is among the biggest obstacles for the world’s central bankers. In August, for example, higher prices meant that gasoline costs accounted for half of the increase in the US consumer price index.

“The Federal Reserve should be aware of them and their influence in markets,” said Rebecca Babin, a senior energy trader for CIBC Private Wealth in New York.

“CTAs can create these fractures — periods of time when we’re trading away from fundamentals,” Babin said. And while those moments may be short-lived, the ensuing price swings “read through into the broader economic world in a lot of different ways,” she said.

Big Swings, Big Profit

While algorithmic CTAs add much-needed liquidity to the market, their trading strategies can amplify daily swings to an extreme. In 2022, when CTA trading volumes rapidly expanded, New York oil futures posted a more-than $2 daily move 242 times. That’s 150% higher than the historical average since 2000, according to Bloomberg calculations.

But what’s so surprising about the continued volatility in 2023 is that it’s come without the major shock to supplies that followed Russia’s invasion of Ukraine. While Israel’s conflict with Hamas set markets on edge, it’s not yet had any major impact on oil flows. And rallies buoyed by production cuts from the Organization of Petroleum Exporting Countries and its allies have been undercut by CTA activity.

The unpredictability of this year’s market swings haven’t been kind to human traders, many of whom are making less money on oil than they did last year when they raked in record gains, according to market participants.

CTAs, by contrast, have been booming — notching three straight years of gains in energy markets, according to Stephen Roseme of Bridgeton.

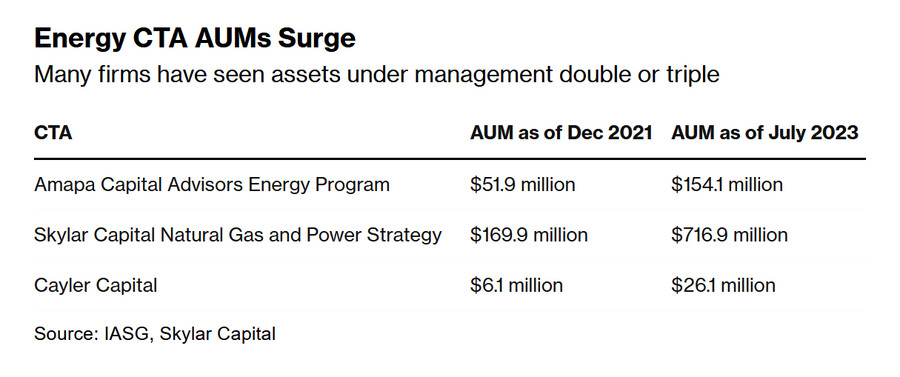

And many CTAs are expanding. Paris-based Capital Fund Management says its CTA’s assets under management (운용 자산) jumped to $3.8 billion in July 2023 from $2.4 billion in December 2021. Amapa Capital Advisors LLC and Skylar Capital Management are among CTAs that have doubled or tripled assets under management in less than two years, CTA advisory firm IASG reports. The largest CTAs in energy are Man AHL, Gresham, Lynx and AlphaSimplex, according to BarclayHedge, but their exact volumes are difficult to quantify.

Man Versus Machine

The beauty of algorithmic CTAs, according to the humans behind them, is that they’re untainted by bias and impulse — they’re predominately mathematical. That approach, of course, is anathema to many in commodities, where man’s dominion over nature, and markets, is foundational.

“Every trader thinks they’re the best. Every trader thinks they have the edge,” says Brent Belote, who gave up an oil trading career at the biggest US bank, JP Morgan Chase & Co, to launch his own CTA in 2016.

Trusting a machine didn’t come naturally to Belote. Although he’s built six algos, he initially found himself trading alongside them. After all, he had years of expertise that the computer did not.

When Russia invaded Ukraine in early 2022 and Brent crude futures skyrocketed 35% to trade above $120 a barrel, Belote wanted desperately to direct his algos. It was a subzero morning in Jackson, Wyoming, when he rose to check on his models – but he decided not to intervene. In the aftermath of the invasion, his firm, Cayler Capital, returned 25% to investors, he said. That compares with 1% for Bloomberg’s hedge fund index.

“The numbers don’t lie,” said Belote.

Brent Belote

Photographer: Natalie Behring/Bloomberg

Not ‘Flash Boys’

CTAs themselves aren’t new — they’ve been around since the early days of futures trading. And since 1984, they’ve had to register with the National Futures Association. They typically enjoy a lower barrier to entry than hedge funds, which can trade a wider variety of securities and require more initial capital. (CTA ≠ 헤지 펀드)

They’re not really the “Flash Boys” of futures, though. CTAs, unlike high-frequency traders, aren’t typically profiting from the speed at which they move. Instead, they mostly make money on indicators fueled by trends. And they’re active in equities and commodities alike through futures and options. (CTA = 추세 추종 매매 ≠ 초단타 매매)

Markets for commodities, however, differ from equities in many important respects. For example, while the stock market evolved as a way to raise capital, commodities futures markets have traditionally been a place for producers and buyers to hedge their price risk. (상품 선물 시장의 본래 목적은 위험 관리. 즉, 생산자와 구매자들이 원자재 가격의 변동성을 헷지하기 위해 상품 선물 시장을 이용)

Born From the Crash

How did CTAs come to become so dominant? Like many current phenomena, the answer starts in the depths of the pandemic.

As shutdowns engulfed the world in 2020, fuel consumption collapsed by more than a quarter. All hell broke loose in the crude market. The benchmark US oil price briefly dropped to minus $40 a barrel and investors were in wholly new territory. Some funds that took longer-term views based on supply-and-demand fundamentals quickly pulled out.

Such bear markets proved to be “extinction events” for traditional funds, which made way “for algo supremacy,” the bulk of which are CTAs, said Daniel Ghali, senior commodity strategist at TD Securities. Russia’s invasion of Ukraine gave the CTAs another foothold. Spiking volatility in the futures market drove many remaining traditional investors to the exits, and open interest (미결제 약정) in the main oil contracts tumbled to a six-year low.

That coincided with the collapse of another source of futures and options trading: oil-production hedging. During the heyday of shale expansion about a decade ago, drillers would lock in futures prices to help fund their growth. But in the aftermath of the pandemic-induced price crash, a chastened US oil industry increasingly focused on returning cash to investors and eschewed hedging, which can often limit a company's exposure to the upside in a rising market. By the first quarter of this year, the volume of oil that US producers were hedging by using derivatives contracts had fallen by more than two-thirds compared with before the pandemic, according to BloombergNEF data.

The recent wave of dealmaking by US oil producers (미국 석유 메이저 기업들의 M&A) threatens to further accelerate the decline in hedging. And it’s highly likely that CTAs will continue to fill the vacuum left by those traditional market players.

In some ways, the rise of the CTAs is just starting. That’s evident to Bouchouev of NYU, who says that his students consider working at the funds a “dream job.”

“CTAs are an example of how technology is getting into our space,” he said. “You’d be a dinosaur after a while if you reject it.”

— With assistance from Jennifer A Dlouhy and Michael Roschnotti

user error : Error. B.