-

[경제] (Bloomberg) Japan’s Fading Rally Drives Some Investors to Cheap China Shares2023.11.04 PM 08:47

블룸버그 기사 요약

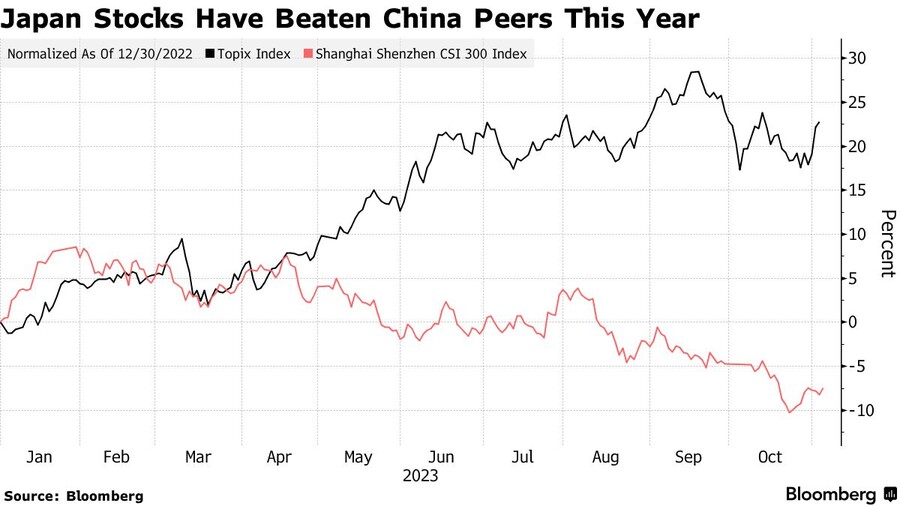

올해 일본 증시(TOPIX)는 경제 성장률 증가 및 기업 지배 구조 개선 노력으로 좋은 성과를 거뒀음

반면 중국 증시(CSI 300)는 경제 성장 둔화와 부동산 시장 침체로 인해 부진한 모습

1) 하지만 일본 증시는 정점을 지났을 가능성이 있음

① 수출 전망 약화

세계 각국이 인플레를 잡기 위해 금리 인상에 나서면서 글로벌 수요 전망이 약화

TOPIX 기업의 25%가 수출에 의존하는데, 이는 CSI 300에 비해 높은 비중

② 미국 증시와 높은 상관관계

TOPIX는 S&P 500과 높은 상관관계를 가짐

S&P 500은 지난 달에 조정장에 진입했었음

반면 CSI 300과 S&P 500은 상관성이 낮음

③ 글로벌 투자자 추가 매수 여력 낮음

글로벌 투자자들의 일본 주식 비중은 지난 10년 대비 매우 높은 수준

따라서 추가 매수 여력이 제한적임

일본 은행이 완화적 통화 정책을 종료하면 (엔화 강세로) 일본 증시에 역풍이 불 수 있음

엔화는 올해 거의 13% 하락했고 30년 만의 저점에 가까워서 충분히 상승할 수 있는 여지가 있음

2) 중국 증시에 유리한 요인들

① 실적 전망

CSI 300의 향후 12개월 실적 성장률은 22%로 추정됨

반면 TOPIX의 예상 실적 성장률은 5%에 불과함

② 밸류에이션

CSI 300의 12MF PER은 10.5배 (5년 평균 PER 12.4 대비 낮은 수준)

역사적 평균 대비 저평가 상태이기 때문에 향후 반등의 여지가 있음

반면, TOPIX의 12MF PER은 14.3배 (5년 평균 PER과 비슷한 수준)

③ 정책적 지원

중국 정부의 경제/증시 부양 정책들

향후 조정장이 와도, 글로벌 투자자 비중이 낮고 저평가된 중국 증시는 다른 아시아 국가 대비 잘 버틸 가능성이 있음

3) 다만, 중국 증시가 일본 증시 대비 상대적으로 더 나은 성과를 거둘 수도 있지만, 지정학적 위험 등으로 인해, 종목 선택은 신중하게 해야할 것

======================================================================

Heavy p-ositioning by global funds poses risk for Japan shares

There are many opportunities in the Chinese market, M&G says

By John Cheng and Ishika Mookerjee

2023년 11월 4일 오전 9:00 GMT+9

Headwinds are growing for Japanese equities including deteriorating global growth and concern the era of yen weakness that has bolstered exporters’ earnings may be nearly over as the central bank comes under pressure to tighten policy.

Conversely, optimism is building that Beijing’s efforts to bolster the economy and local equity markets will help end a slump that has made Chinese equities among the world’s worst performers this year. Historically low valuations are also set to lure bottom fishers.

“The relative outperformance in the next 12 months will come from the likes of China or China-centric type of economies,” said Jun Bei Liu, a fund manager at Tribeca Investment Partners Pty in Sydney. “Japan is an easy one” to fund the trade after its huge outperformance this year, she said.

Japan’s Topix index has jumped 23% in 2023, heading for its best year in a decade, as economic growth accelerated and efforts to improve corporate governance lured investors. Meanwhile, China’s benchmark CSI 300 has slumped 7.4% as a faltering economy dashed optimism over the nation’s reopening from Covid restrictions and the ailing property market has yet to recover.

There are signs Japan’s outperformance may have peaked.

The Topix is already more than 4% off its high for the year as rapid global interest-rate hikes worsen the outlook for external demand, which would hurt Japan’s industrial powerhouses. Export-reliant industrials make up about a quarter of the index, a larger proportion than in the Chinese benchmark.

Japanese stocks are also smarting from their high correlation with the S&P 500 Index, which entered a technical correction last month. The Topix and S&P 500 have had a weekly correlation of 0.57 over the past decade, while that between the CSI 300 and S&P 500 was just 0.1. A reading of 1 would mean the two moved in lockstep.

Another risk for Japanese shares is the heavy p-ositioning by global funds. Overseas investors have bought a net $30.7 billion of local stocks this year through Oct. 27, on track for the biggest year of purchases since 2013.

“Global funds are highly exposed to Japanese equities, much more so than in the last decade,” HSBC Holdings Plc strategists Herald van der Linde and Prerna Garg wrote in a research note last month. “So there’s limited room to increase their holdings.”

The bank is underweight Japan and overweight mainland China, they said.

Yen Danger

Any downdraft in Japanese stocks may accelerate if the yen starts to strengthen. The currency has plenty of room to appreciate as it’s tumbled almost 13% this year and is close to a three-decade low.

While the Bank of Japan disappointed yen bulls this week by only modestly tweaking its yield-curve-control policy, it did take a step in that direction and a more substantive move would boost the currency.

Among positive factors for Chinese equities is the attractive outlook for earnings. Companies in the CSI 300 Index will see earnings grow an average 22% over the next 12 months, according to forecasts compiled by Bloomberg. That compares with just 5% for constituents in Japan’s Topix.

Valuation metrics also suggest Chinese equities have room to rebound. The CSI 300 Index is trading at 10.5 times forward earnings, below its five-year average of 12.4 times. The Topix trades at 14.3 times, in line with its five-year mean.

“In a correction, China should hold better than other markets in Asia due to light p-ositioning and cheap valuations,” said Luca Castoldi, a senior fund manager at Reyl Group in Singapore. Japan on the other hand is likely to follow the US going forward, he said.

Reyl is looking to add to its holdings in China while being short Japanese stocks and long the yen, he said.

Choose Carefully

Even though there are plenty of reasons for Chinese shares to outperform their Japanese peers, seasoned investors say the challenging global investment landscape still calls for careful stock picking.

“There are a lot of opportunities in the Chinese market because it is such a deep market, but you need to stay selective,” said Fabiana Fedeli, chief investment officer for equities, multi asset and sustainability at M&G Plc in London. The money manager has been increasing p-ositions in China in recent months, she said.

user error : Error. B.