-

[경제] 공매도 금지 첫날 과열…'중장기적으로 외국인 순매도 가능성'2023.11.06 PM 01:32

(서울=연합뉴스) 임은진 이민영 기자 = 증시 안정을 위해 주식을 빌려 파는 공매도가 금지된 첫날인 6일 국내 증시가 과열 양상을 보이고 있다.

시장에서는 이번 조처로 단기적으로는 수급에 긍정적인 영향을 미치겠지만 중장기적으로는 외국인 자금 이탈이 발생할 가능성이 있다고 보고 있다.

◇ "숏커버링으로 단기 수급엔 긍정…중장기적으로 외국인은 순매도"

공매도가 금지되면서 거래 규모가 컸던 외국인 투자자가 얼마만큼 숏커버링(환매수)에 나설지 주목된다.

일단 증권가에서는 국내 증시가 반등하면서 기존 공매도 물량의 숏커버링이 발생해 단기 수급에 긍정적인 영향을 줄 수 있을 것으로 기대하고 있다.

특히 그간 공매도 거래 비중이 컸던 종목을 중심으로 수급이 개선될 것으로 보고 있다.

한지영 키움증권 연구원은 "공매도 금지의 부작용이 출현해도 이를 체감하기까지는 시간이 소요될 것으로 예상되나 업종이나 개별 종목에서는 이번 주부터 공매도 금지 효과를 체감할 수 있다"고 내다봤다.

숏커버링 효과로 공매도의 선행 지표라고 할 수 있는 대차거래 규모도 감소할 것으로 보인다.

대차거래는 주식을 빌리는 것으로, 국내에서는 무차입 공매도가 금지돼 있어 주식을 빌려 매도한 뒤 재매입해 갚는 공매도를 위해서는 대차거래가 필수다.

대차거래의 경우 주식 차입뿐 아니라 ETF 설정과 환매 등을 위한 주식 대여나 결제 목적의 증권 차입 등 다양한 목적으로 시행되지만, 공매도 금지로 차입 목적의 대차거래가 감소할 수 있어서다.

다만 중장기적으로는 외국인의 증시 이탈 가능성도 점쳐진다.

실제로 삼성증권이 2023년 3월 공매도 금지 이후에 대한 영향을 분석한 자료에 따르면 조사 기간인 2020년 3월 16일∼6월 12일 동안 개인 투자자는 순매수를 기록했지만 외국인 투자자는 순매도 했다.

삼성증권은 보고서에서 "일반적으로 공매도의 주요 주체로 외국인 투자자를 지목하지만, 외국인 투자자들에게서는 공매도 금지 기간 공매도의 숏커버링 흔적보다 국내 주식에 대한 지속적인 매도 압력을 확인할 수 있었다"며 "오히려 개인 투자자의 공세적인 주식 매수가 코로나19 사태에서 국내 주식 시장의 반등을 주도했다"고 말했다.

나정환 NH투자증권 연구원은 "오늘 증시는 원래 바닥에서 올라가는 상황인데 공매도를 금지하면서 외국인이 숏포지션 줄이면서 동시에 숏커버링에 나서는 효과 때문에 주가 상승폭이 확대되고 있다"면서 "단기적으로는 외국인이 매수 우위 보일 가능성이 크다"고 내다봤다.

다만 그는 "장기적으로 봤을 때 주식 시장의 투명성 저해라는 관점에서 MSCI 선진국 편입 가능성이 떨어지는 등 좋지 않은 영향을 끼칠 수 있다"며 "기존 공매도 잔고는 연초 이후에 이미 많이 쌓인 상황이기에 줄어들 수밖에 없다. 한 2∼3주 정도는 감소할 것"이라고 말했다.

◇ 첫날 증시에는 호재…코스닥은 과열 양상까지

일단 이날 오전 11시 15분 현재 코스피는 4% 가까이 상승하고 있고, 코스닥도 5%를 훌쩍 넘기며 오르고 있다. 이에 코스닥시장에서는 사이드카가 발동되기도 했다.

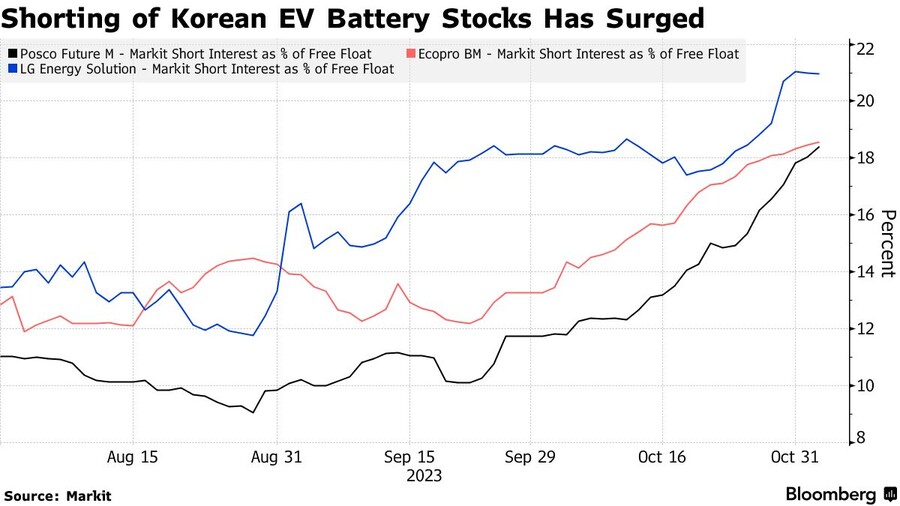

삼성전자와 LG에너지솔루션, 에코프로비엠과 에코프로 등 시가총액 상위주 모두 오르고 있다.

주가 상승은 이차전지와 호텔신라 등 공매도 비중이 높은 종목이 견인하고 있다. 공매도 비중은 총주식 거래대금에서 공매도 거래대금이 차지하는 비율을 뜻한다.

유가증권시장에서는 LG에너지솔루션(22.39%), POSCO홀딩스(19.41%), 포스코퓨처엠(29.00%) 등이, 코스닥시장에서는 에코프로비엠(29.35%), 에코프로(29.98%) 등이 두 자릿수 증가율을 보이고 있다.

한국거래소에 따르면 공매도 비중 상위 1∼5위 종목인 호텔신라(4.77), 롯데관광개발(4.80%), SKC(13.59%), 후성(7.58%), 두산퓨얼셀(9.52%)도 오름세다.

이 같은 강세는 그간 공매도 거래가 상대적으로 많았던 외국인이 주도하는 것으로 보인다.

실제로 이날 장 초반 외국인은 순매도하고 있는 개인과 기관과 달리 국내 주식을 사들이고 있다.

외국인은 유가증권시장에서 3천457억원어치, 코스닥시장에서는 1천466억원어치 순매수를 기록하고 있다.

김대준 한국투자증권 연구원은 "지금까지 특정 이슈로 인해 공매도 잔고가 많이 쌓였던 종목들이 단기적으로 가장 빠르게 움직일 것"이라며 "코스피200 종목 중에서는 펀더멘털과 관계없이 호텔신라, 롯데관광개발, SKC의 반등 가능성이 높다"고 진단했다.

이경민 대신증권 연구원은 "아직 공매도 금지 영향으로 주가가 상승했다고 보기는 이른 측면이 있다"며 "그간 낙폭이 컸던 종목은 반등세를 보이고 있지만, 시장 전체에 대한 호재인지는 좀 더 지켜봐야 한다"고 말했다.

========================================================

(Bloomberg) Short-Selling Ban Sparks Biggest Korea Equities Rally Since 2021

Kospi rises 4.1%, boosted by shorted stocks like LG Energy

Ban ‘unusual’ in absence of a financial crisis: Eugene’s Huh

By Youkyung Lee

2023년 11월 6일 오전 9:05 GMT+9

Updated on 2023년 11월 6일 오후 1:07 GMT+9

South Korean stocks jumped after regulators reimposed a full ban on short-selling for about eight months, a controversial move that they said was needed to stop the illegal use of a trading tactic deployed regularly by hedge funds and other investors around the world.

The move may have been to appease retail investors who have complained about the impact of shorting — the selling of borrowed shares by institutional investors — ahead of elections in April, several market watchers said. However, it could deter participation by foreign funds in the $1.7 trillion equity market and complicate Korea’s bid to seek a developed-market status in MSCI Inc.’s indexes.

The Kospi jumped as much as 4.1%, the most since January 2021. Overseas investors were big buyers on a net basis, indicating that funds were covering short p-ositions. Stocks that had recently witnessed an increase in short selling — including LG Energy Solution Ltd. and Posco Future M Co. — were among the biggest contributors to the benchmark’s advance. The small-cap Kosdaq Index surged as much as 6.2%, the most since March 2020.

The Financial Services Commission said on Sunday that new short-selling p-ositions will be prohibited for equities on the Kospi 200 Index and Kosdaq 150 Index from Monday through the end of June 2024. The decision doesn’t impact existing p-ositions. While pandemic-era curbs on the practice had been lifted for those two gauges in May 2021, the ban had remained in place for some 2,000 stocks.

“This policy reversal with respect to short selling is unwarranted at the current time,” said Wongmo Kang, an analyst at Exome Asset Management. “Many people view it as a political move aimed at next year’s general election,” he said, adding that the Korean market tends to be “heavily influenced by retail investors.”

South Korea is set to conduct general elections for the National Assembly in April and public perception of short-selling remains deeply negative in the nation. Some ruling party lawmakers urged the government to temporarily end stock short-selling in response to demands by retail investors, who have staged protests against the tactic and also made sporadic coordinated attempts to drive gains in stocks targeted by short sellers.

Most short-selling in South Korea is conducted by institutional investors. However, it accounts for a tiny portion of the market — about 0.6% of the Kospi’s market value and 1.6% of the Kosdaq’s, according to exchange data.

Naked Shorts

Lee Bokhyun, governor of the Financial Supervisory Service, refuted the view that the ban was politically motivated, adding that the suspension was necessary to protect retail investors and improve the short-selling mechanism. The ban was “inevitable to introduce an advanced short-selling system,” he was cited as saying by Yonhap Infomax.

Sunday’s announcement comes just days after the financial watchdog said it plans a comprehensive probe into short-selling trades by global investment banks, with a view to root out the practice of naked short-selling, which is illegal in South Korea. Earlier in October, the FSS proposed the imp-osition of record fines on two global banks for “routinely and intentionally” engaging in naked short-selling.

The so-called naked variety of the trade involves shorting shares without borrowing them first.

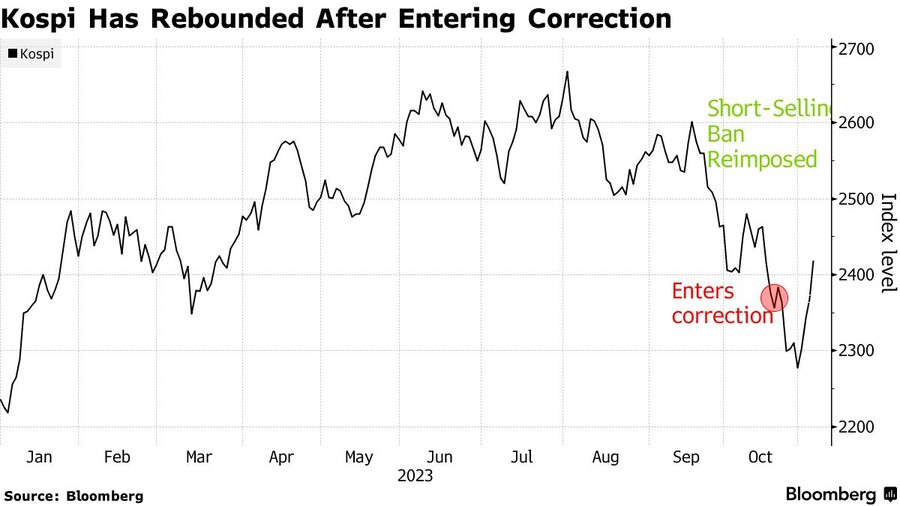

The Kospi surged earlier this year on frenzied buying of electric-vehicle battery names and chip stocks related to the artificial intelligence theme. Concerns over geopolitical tensions and high interest rates reversed the rally in recent months, driving the benchmark into a technical correction and nearly erasing its gain for the year.

The gauge is currently up about 10% in 2023 versus a 2.5% advance in the broader MSCI Asia Pacific Index.

The latest ban is “unusual” as authorities are comprehensively prohibiting short selling at a time when there is no major external risk, said Huh Jae-Hwan, an analyst at Eugene Investment & Securities. South Korea had banned short selling during the Global Financial Crisis in 2008, amid the euro-zone debt crisis and the US sovereign downgrade in 2011, and then again during the start of the pandemic in 2020.

While regulators argue that naked short-selling inhibits fair price formation and hurts confidence, some observers say broad outright bans make the market less transparent and therefore less attractive. Some also say the restrictions may keep the market from being upgraded in MSCI indexes.

“It does compromise their status and certainly would hold them back from achieving developed market status,” said Gary Dugan, chief investment officer at Dalma Capital Management Ltd. “Given that there is an immediate ban there will be an initial sharp move higher in stock prices of companies that have had some short selling,” but the impact may be limited given low levels of short p-ositions in the overall market, he said.

A spokeswoman for MSCI said the index provider does not comment on potential future reclassifications. South Korea needs to take the politically sensitive step of fully lifting curbs on stock short selling to ensure inclusion in a key global index, the head of the country’s securities exchange said in an interview earlier this year.

“There is a possibility that international investors may lose trust and opportunity in the Korean market,” Exome Asset’s Kang said. “Without the ability for investors to express a view that markets and individual stocks are ‘mispriced’ to the upside, stock markets lose long term credibility on the world stage.”

user error : Error. B.