-

[경제] (블룸버그) 2024년 강력한 출발을 보이는 도쿄 증시, 34년 만의 고점 돌파2024.01.13 PM 07:38

블룸버그 기사 요약 (ChatGPT)

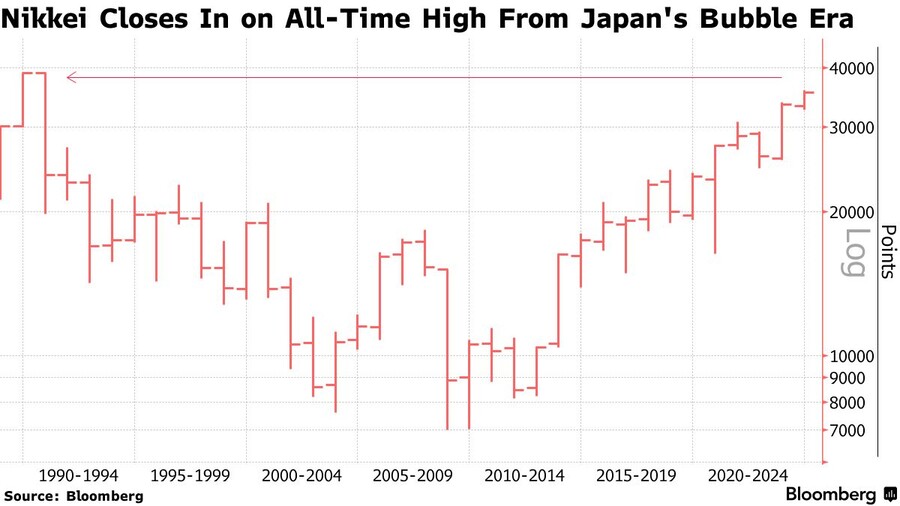

도쿄 증시는 2024년 들어 다른 주요 시장보다 강력한 출발을 보이며 34년 만의 고점을 돌파했습니다. 투자자들은 일본이 디플레이션을 극복하고 있다는 데 낙관적이며, 올해 니케이225 지수가 약 10% 상승하여 1980년대 거품 경제 이후 최고치에 근접할 것으로 예상하고 있습니다.

지난해 일본 주식은 큰 상승세를 보였으며, 디플레이션 종식이 명확해지면서 시장 분위기가 전환되고, 기업들이 주주 가치 창출에 더욱 집중하면서 이러한 현상이 나타났습니다. 과다 평가에 대한 우려에도 불구하고, 토픽스 지수는 기대 수익률의 약 15배로 거래되고 있으며, 대부분의 투자자들은 싸지도 비싸지도 않은 수준이라고 평가하고 있습니다.

1980년대 거품 시대와의 비교는 오늘날 더 낮은 평가를 보여주는 다른 풍경을 보여줍니다. 1980년대 후반에는 PBR (주가 순자산 비율)이 5.4배였지만, 현재는 1.4배이며, PER (주가 수익 비율)은 70.6배였지만, 현재는 훨씬 낮은 수준입니다. 현재 시장은 버블 붕괴 시기보다 비교적 저평가되어 있다고 할 수 있습니다.

일부 투자자들은 단기적으로 시장이 과도 매수(overbought)되었다는 점에 대해 신중한 입장을 취하고 있지만, 다른 투자자들은 긍정적인 변화의 현실을 믿고 있습니다. 일본 기업들은 자본 효율성을 향상시키고 주가를 부양하라는 압력을 받고 있습니다. 이는 미래 배당 성장에 대한 낙관론을 불러 일으키고 있습니다. 잠재적인 시장 조정 가능성에도 불구하고, 많은 투자자들은 긍정적인 장기 구조적 변화로 인해 일본 주식의 포트폴리오 비중 재평가에 기회를 보고 있습니다.

====================================================================================

(Bloomberg) Tokyo Stocks Find Their Mojo as Bubble-Era Highs Draw Nearer

■ Some see all-time highs in view, signaling 10% rally this year

■ Valuations are far below dizzying heights of late 1980s

By Hideyuki Sano and Aya Wagatsuma

2024년 1월 13일 오전 8:00 GMT+9

The roaring start to 2024 for Japanese equities looks to be on far more solid ground than last time stocks reached these lofty levels as investors bet the country is finally escaping deflation.

Gains in Japan’s two main indexes have outpaced all other major markets during the first two weeks of trade, reaching fresh 34-year peaks. That’s stoking the bullish view that the bellwether Nikkei 225 Stock Average is primed to gain almost 10% as soon as this year and reclaim its all-time record hit at the height of the bubble economy in 1989.

“There’s a strong possibility that stocks will go above their highs by the end of this year,” said Shigeharu Shiraishi, representative director at Know’s i-land Asset Management Inc., and an industry veteran who had first-hand experience with investing in Japanese stocks during the period of over-inflated asset prices in the late 1980s.

This month’s spurt surprised many investors who were expecting stocks to consolidate after last year’s chunky gains, leading them to entertain the possibility that the market is far stronger than thought. It’s fueling bets that now’s the time to rotate more money out of markets such as China, with the bullishness overshadowing concerns that Japanese equities might be overbought.

“Last year was a watershed for Japanese stocks,” with world-beating rallies of more than 25%, said Tetsuro Ii, chief executive of Commons Asset Management. “The end of deflation has become clearer, and companies are starting to look to shareholders more,” he said. “These are big stories that will not go away in just a year or so.”

With the Topix trading at around 15 times expected earnings, in line with its average over the past 10 years, most investors consider the market to be neither cheap, nor expensive. That multiple is about 17 for global stocks.

It’s a different world now compared with the last time Japanese shares were at these levels. In the late 1980s, the price-to-book ratio - a measure of a company’s valuation - was 5.4 times, compared with 1.4 now. The price-to-earnings ratio was a dizzying 70.6 times.

At the time, investors justified ridiculously high valuations on the grounds that Japanese companies had a strong source of revenue in the way of ever-soaring asset values. Real estate prices were climbing at an unbelievable pace in the 1980s — talk had it that the price for the land in the Imperial Palace might be worth more than the state of California. Land prices now are just starting to rise after decades of sluggishness.

Japan was comfortably the world’s second-biggest economy, and some speculated it might challenge the US’s dominance. It was overtaken by China more than a decade ago and now risks sliding into fourth place. The internet didn’t exist in daily life during Japan’s bubble era, and iPhones wouldn’t come out for another couple of decades.

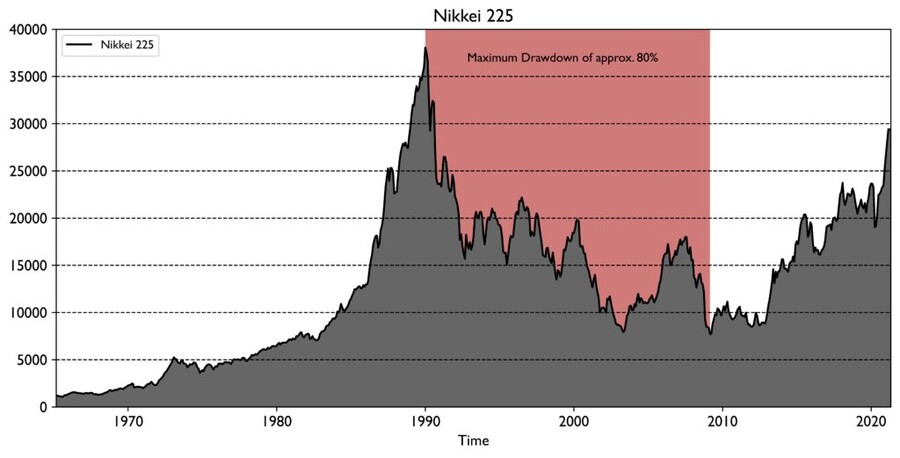

The Nikkei’s previous rally to the 1989 high was followed by one of the worst market collapses in history. The measure shed as much as 82% from its peak through to the financial crisis almost two decades later. That’s close to losses of about 90% for the US Dow Jones Industrial Average during the Great Depression.

Shiraishi said he learned in the 1990s that assets that were overpriced and overbought have to fall. “Japanese equities today are extremely undervalued compared to their levels at the time,” he said.

Some think the market is some way off reaching new highs, given that Japan’s earnings growth for 2024 is expected to be in the low single digits.

In the very near term, the market is already in overbought territory, with the Nikkei’s relative strength index rising above a key level of 70 that usually signals overheating.

In addition, “policy expectations for both the Federal Reserve and the Bank of Japan are likely to be readjusted for higher yields into March meetings and stock prices are likely to readjust,” said Naka Matsuzawa, chief strategist at Nomura Securities Co.

Still, despite the risks, many investors think the changes that are taking place are real.

A growing number of Japanese companies have already promised to make the largest wage hikes in decades this year, keeping investors positive about the inflation outlook despite recent signs of softness in domestic consumption.

Japanese companies are under pressure from the stock exchange to improve capital efficiency and share prices. That is likely to mean their dividend payments will grow further, even after more than doubling in the past decade.

Any correction over the next quarter or two “would be an excellent opportunity for investors to re-evaluate their portfolio weightings to Japanese equities, considering the extremely positive longer-term structural changes underway,” Lazard Asset Management said in a report this week.

user error : Error. B.